Mortgage Rates Today: Today's Dip, the 30-Year Outlook, and Your Refinance Window

# The Future of Homeownership: Why Today's Mortgage Rate Dip is More Than Just Numbers

Alright, let's talk about something truly exciting, something that’s buzzing right now, not just in the financial pages but in the very fabric of our collective dreams: homeownership. For what feels like an eternity, the housing market has been a labyrinth of uncertainty, a high-stakes game where the house always seemed to win. But folks, I’m seeing a shift, a genuine, palpable moment of opportunity, and it’s all tied to something as seemingly mundane as today’s mortgage interest rates.

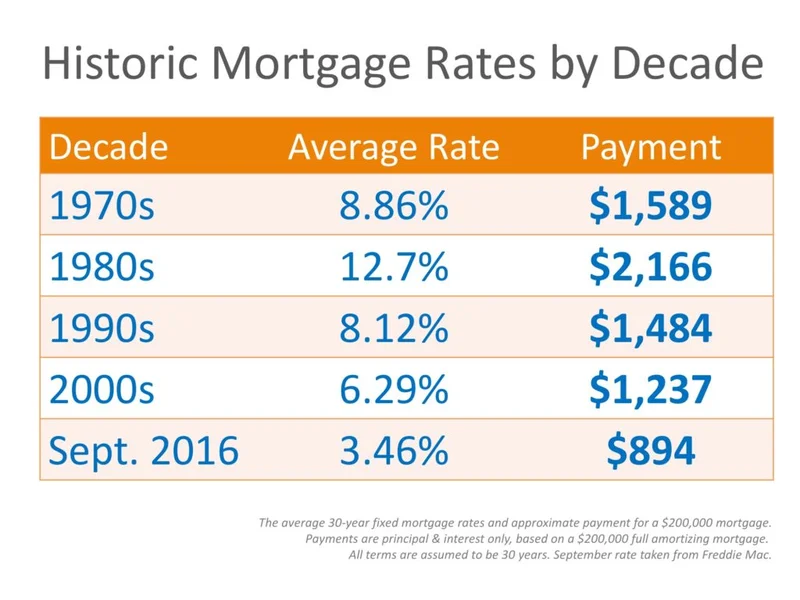

You see, it’s easy to get lost in the sea of percentages and basis points, to dismiss a drop here or a rise there as just market noise. But when you zoom out, when you truly look at the trajectory, what’s happening with mortgage rates today isn't just a blip on the radar; it’s a potential paradigm shift. We’re talking about the average 30-year fixed-rate mortgage nudging down to 6.03% APR as of November 27, 2025 – a whisper lower than yesterday, a quiet hum compared to a week ago, and a full 51 basis points lower than last year. And the 15-year fixed-rate and 5-year adjustable-rate mortgage rates? They’re following suit, shedding points like old skin. This isn't just about saving a few bucks; it’s about unlocking potential, about making the impossible feel, well, possible again.

The Unseen Revolution in Your Wallet

This isn't a dry economic report; this is a story about human potential, about families finally seeing a glimmer of hope. When I first started digging into the underlying currents pushing these mortgage rates down, I honestly just sat back in my chair, speechless. It’s not simply the numbers, though a 6.03% average for a 30-year mortgage rate is certainly a sight for sore eyes after years of chasing 7% and beyond. No, the real magic, the true breakthrough, lies in the implications.

We've been hearing the whispers for a while now, haven't we? The Federal Reserve, that colossal engine of our financial landscape, is looking at another rate cut in December. This isn't just speculation; influential figures like New York Fed president John Williams and San Francisco Federal Reserve president Mary Daly have all signaled their support. This growing consensus, fueled by signs of a weakening labor market – which, I know, sounds counterintuitive, but in this context, it often means the Fed feels more comfortable easing up – is like the slow, deliberate turning of a massive ship. And that ship is heading straight for lower borrowing costs for us.

Think about it: hundreds of thousands of homeowners are currently saddled with mortgage rates around 7%. For them, this isn't just a rate dip; it’s a golden ticket, a chance to refinance and breathe easier, to free up hundreds, even thousands, of dollars annually. That’s not just money saved; that’s a child’s college fund getting a boost, a long-postponed home renovation finally happening, or simply the peace of mind that comes from a lighter monthly burden. It’s like discovering a hidden spring in a parched desert, offering vital sustenance when you thought you were completely out of options.

What this means for us is a chance to re-evaluate our financial landscapes, but more importantly, what could it mean for you? Have you been on the sidelines, dreaming of a first home, or agonizing over a loan you snagged during the peak? This is your moment to lean in, to ask those hard questions: "What are my options now? Could I finally escape that 7% trap?" This is where the rubber meets the road, where abstract market movements translate into tangible, life-altering possibilities for everyday people. And that, my friends, is why I get so incredibly fired up about this.

Navigating the Tides: Your Power in the Equation

Now, I hear the skeptics. "It's just a small dip, Dr. Thorne! The market's too volatile!" And yes, you're right, the market is a tempestuous beast, influenced by everything from global economies to national elections – in simpler terms, all the big stuff you can't control. But here’s the thing: while you can’t control the global economy or the Fed's next move, you have immense power over your personal position in this equation.

This is where individual agency truly shines. Your credit score, your down payment, the type of loan you choose – these are the levers you can pull. A solid credit score, a hefty down payment, choosing a primary residence loan over an investment property loan – these aren't just details; they're your personal armor in the quest for the best current mortgage rates. It's a bit like preparing for a marathon; you can't control the weather on race day, but you can control your training, your diet, your gear. The better prepared you are, the better your outcome, regardless of the external conditions.

And here’s a thought leap for you: remember the early days of the internet? People scoffed, saying it was just a fad, a niche for academics. They missed the fundamental shift in how information would flow, how connections would be made. Similarly, some might dismiss these mortgage rates news as temporary fluctuations, but they're missing the profound shift in access to capital that could ignite a new wave of homeownership and refinancing. This isn't just about a good week; it’s about a potential turning point that could echo for years. We're seeing chatter on forums, like one I spotted on a finance subreddit, where someone excitedly posted, "This is it, folks! I locked in 5.85% today. Don't wait for 'perfect,' just get better!" That's the spirit, the collective hope bubbling to the surface.

Of course, with great opportunity comes great responsibility. As we push for lower rates and easier access, we must also ensure that we're building a sustainable future, not just chasing short-term gains. How do we ensure that these opportunities are equitable, reaching those who need them most, and not just fueling another speculative bubble? These are the crucial, open-ended questions we need to keep asking ourselves as this exciting chapter unfolds.

The Dawn of a New Homeownership Era

The bottom line here is crystal clear: the narrative around homeownership is changing, and it's changing fast. What was once a distant dream for many, a financial Everest, is slowly but surely becoming more accessible. The continuous downward pressure on interest rates, the anticipation of further Fed cuts, and the sheer power of shopping around for the best mortgage rates today – these forces are converging to create a truly remarkable moment. Don't let the headlines blur the vision; look beyond the daily fluctuations and see the bigger picture. This isn't just about numbers; it’s about empowering individuals, fostering stability, and building a more secure future, one home at a time. It’s time to lean in, to explore, and to embrace the possibilities.